Money is complicated in more ways than we realize. Most advice speaks to numbers, but financial therapist Amanda Clayman gets to the root of the problem: the underlying needs, emotions, and behaviors that drive our financial choices.

Dilemma: You’re in a relationship with someone who grew up in circumstances you might describe as “privileged”—or wealthy—with access to second and third homes, private chefs, and what seems like a never-ending trust fund. You came from a middle-class home where vacations happened once every decade. The differences weren’t apparent at first, but as you move forward with day-to-day life, from dinners out, to expensive, spontaneous splurges, the tension is starting to build. Can two people from different financial backgrounds be happy together?

Amanda Clayman: When it comes to money and relationships, difference is the norm. It may not sound very romantic, but one of our primary motivations for partnering up is to form a team: with our partner, we get a stable source of support; we have a shared vision and a shared effort to achieve that; and we can divide up tasks and specialize, so each person doesn’t have to be and do all of the things.

Here’s the secret: The strongest teams are not made up of partners who have exactly the same strengths. In fact, our subconscious has a way of attracting us to someone who has a different approach and different point of view, because they have the potential to contribute something that’s needed for a more balanced system.

When working with couples, I define a healthy financial decision-making process model as one that has five characteristics:

- Equal (both partners have the same amount of power)

- Inclusive (both participate)

- Transparent (both have access to information)

- Sustainable (it is not unfairly burdensome to either)

- Flexible (it can change as needs and priorities shift)

Look at how you and your partner approach financial decisions and management. Where do these characteristics show up? Where are they lacking? For example, do you both have a say in the family budget? Does one person feel tempted to act out and hide their spending, because the other is so controlling? How do you introduce new goals or propose changes to earning and spending?

Get specific about your differences and where they come from

Whether we mean to or not, there’s a lot we assume when we see someone as different. Growing up in a nonaffluent family money culture, it’s possible you were exposed to negative messages about wealth that you may not have even noticed. Maybe you remember your dad grumbling about “that jerk in the Mercedes” who just cut him off. The association between selfish behavior and luxury vehicles was probably not intentional, but that was the message you might’ve picked up: that rich people were jerks and your dad didn’t like them.

When you notice ways that your partner views money and luxury differently than you, try to be as specific as possible about how that difference shows up. When your partner argues that you should buy a designer couch because a quality piece will last longer, do you see that as a valid point, or evidence that this person never had to sleep on a futon in their life? (And futon-sleeping builds character, thank you very much!)

What to do next:When you notice instances of your partner’s behavior that reflect their wealthy upbringing, ask yourself: What associations do I have with these kinds of actions and words? How do I feel in these situations?Are you anxious, angry, resentful? Why?

Identify power dynamics

People who grew up with the status and privilege of wealth may come into relationships with an expectation that their opinions will be heard and their wishes heeded. They may even feel as if wealth serves as confirmation that their opinions and beliefs are correct—and anyone who comes from less money and who thinks differently is simply wrong.

This imbalance of financial power can complicate adult partnerships in a couple significant ways. First, if there are financial strings attached, it can be difficult for the person from wealth to fully separate from their family in order to establish a primary bond with a partner. Money keeps them dependent on their family of origin. If someone grows up in a dominating, autocratic family system, they may also have trouble understanding what appropriate communication, collaboration, and compromise even look like. They see control as “all or nothing.”

One such couple I worked with struggled with how to manage the wife’s trust fund. She saw it as her money and resisted using it for joint responsibilities and goals. She didn’t even want her partner to know how much was in it, as this information was treated as extremely private within the family. She also insisted they spend weeks of the summer at her parents’ beach house, though she herself chafed at this obligation. Her husband resented being shut out of these decisions. He felt like an outsider, powerless to change the dynamic that affected them both. It took a tremendous amount of work to overcome the wife’s conditioning to control information, protect her family of origin, and learn to share decision-making power.

What to do next:Think about how your family system and your partner’s were different. Invite your partner to talk about these differences in a way that is nonjudgmental and focused on exploration as opposed to change. Here are a few starter questions: How did people talk about money in your family? How did financial decisions get made? In what ways do you feel as if this affected you and your financial choices?

Make a money mission statement

You and your partner each bring something necessary and valuable to the relationship—including the different approaches you bring to money. When your partner wants a five-star resort, they might appreciate a reminder that the goal is to pay off student loans, and that a staycation would be better choice this year. Perhaps you even meet in the middle and road trip to a nearby state park. It’s when you each insist on getting “your way” that cooperation and trust break down, and money turns into a source of competition, conflict, and control.

What to do next: To develop cooperation and trust, I recommend creating a Money Mission Statement for you and your partner. Think of it as a way of documenting what you both agree is important in terms of financial values, goals, and process.

Here’s an example:

In our family, we agree that adventure, caring for others, and doing work that we love are central to a happy life. We believe experiences are more important than things, and we commit to a simpler material life so that we can prioritize these values. We make time to think about our money, talk through decisions, and support each other’s dreams and goals. In the future, we hope to have the financial freedom to travel and spend time with family. Saving and investing today are how we can make that hope a reality.

The goal is to shift focus from your differences to what you have in common with your partner. It can also serve as a point of reference, so you recognize when one or both of you make financial choices that are not “on mission.” It is much more neutral to say, “By going out to eat so much, I feel like we’re not sticking with our value of preparing for the future,” as opposed to, “You spend too much on restaurants.”

Money often points us toward ways that we can grow as people. Exploring you and your partner’s differences can help create a more harmonious financial life—and a deeper level of intimacy and commitment.

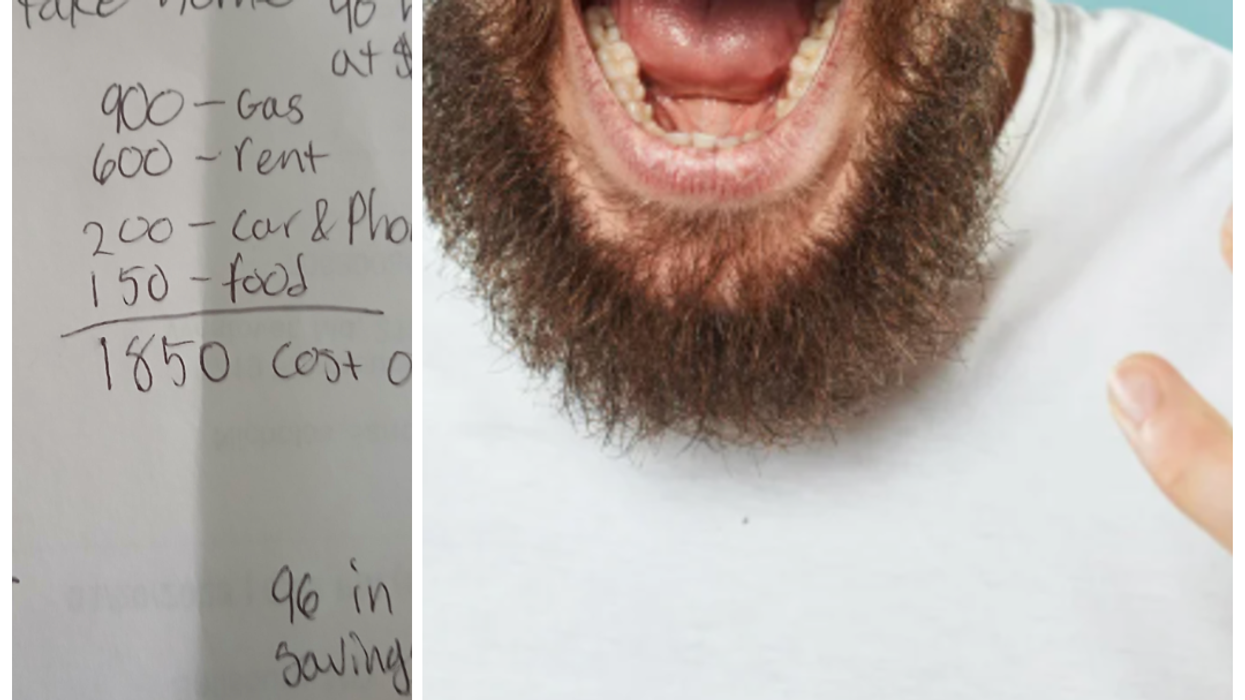

Take home pay is becoming less and less as expenses rise year after year.Photo credit: Canva

Take home pay is becoming less and less as expenses rise year after year.Photo credit: Canva Making bill payments gets harder each year.Photo credit: Canva

Making bill payments gets harder each year.Photo credit: Canva

Representative Image Source: Pexels | Olly

Representative Image Source: Pexels | Olly Representative Image Source: Pexels | Pixabay

Representative Image Source: Pexels | Pixabay Representative Image Source: Pexels | Cottonbro

Representative Image Source: Pexels | Cottonbro Representative Image Source: Pexels | Cottonbro

Representative Image Source: Pexels | Cottonbro Representative Image Source: Pexels | Karolina Grabowska

Representative Image Source: Pexels | Karolina Grabowska Representative Image Source: Pexels | Jonathan Borba

Representative Image Source: Pexels | Jonathan Borba Image Source: Reddit |

Image Source: Reddit |  Image Source: Reddit |

Image Source: Reddit |  Image Source: Reddit |

Image Source: Reddit |

Representative Image Source: Pexels | Pixabay

Representative Image Source: Pexels | Pixabay Representative Image Source: Pexels | Pixabay

Representative Image Source: Pexels | Pixabay Representative Image Source: Pexels | markus winkler

Representative Image Source: Pexels | markus winkler